28

Jun, 2017

28

Jun, 2017

House Financial Services Committee Hearing on Market Structure

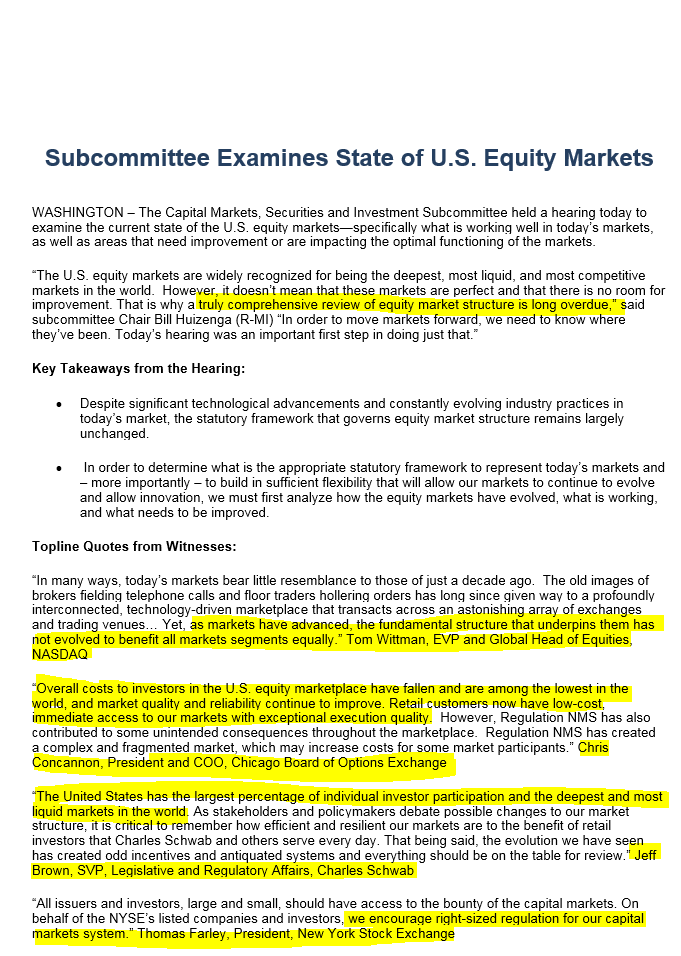

Yesterday the House Financial Committee held a hearing to understand the evolution of today’s equity market structure. They heard testimony from leaders in our financial industry describing how we arrived where we are today, and what problems/issues the equity markets need to address. They heard from:

- Capital Group’s Matt Lyons

- Themis Trading’s Joe Saluzzi

- GTS’s Ari Rubenstein

- Schwab’s Jeff Brown

- NYSE’s Tom Farley

- IEX’s Brad Katsuyama

- CBOE’s Chris Concannon

- Instinet’s John Comerford

- Nasdaq’s Tom Wittman.

You can read the submitted written testimony of each witness in the links above. You can also watch an abbreviated version of Joe Saluzzi’s testimony here.

You can also watch the two panels in their entirety here.

This is the summary of the day’s testimony that the Capital Markets Securities and Investment Subcommittee sent out in an email to their constituents:

The Committee heard testimony throughout the day from Matt Lyons, Joe Saluzzi, and Brad Katsuyama that detailed concerns about Maker Taker, Monopoly Market Data Pricing, and a conflicted insider-run NMS Plan committee. You wouldn’t know it from reading their own summary.

Specifically they heard:

- How asset managers routinely have orders that are significant percentages of the daily trading volume in stocks – as much as 65%.

- How asset managers route through systems that leak. While they use technology intensively, and attempt to plug the leaks, distorted incentives like payment for order flow and maker taker pricing contribute substantially to the leaks.

- How asset managers believe price discovery would be more accurate and robust if more investor orders were represented on the public lit markets, instead of murky dark pools that trade small tiny lots.

- Even regulators have fined firms like Citadel for systemic investor execution abuse, as well as numerous dark pools.

- How the industry needs much better disclosure requirements on where they route orders, and not just where the get ultimately filled.

- How stock exchanges have a monopoly on their own market data, which is required by market participants, and how that data cost has risen 700% in recent years, where data costs have plummeted in virtually every other industry except ours.

- How stock exchanges sell the ability to be faster than the exchanges’ own matching, on their own playing fields where they serve as referee and look the other away.

The Committee seemed to forget including such testimony in their summary, and in fact any testimony, from Mr. Lyons, Saluzzi, and Katsuyama. It’s almost as if, in their role as policy and law-makers, they would be content to conduct a long slow comprehensive holistic market structure review, rather than enact any meaningful reforms in the short term, before markets experience any stress. In other words – stall. This position would be in lockstep with nearly every industry insider who has called for comprehensive and holistic “first do no wrong” reviews since 2010.

This does not surprise us. Selling speed and engaging in payment for order flow is big business. Gander over to Opensecrets.org, and see who the largest contributors to the leadership’s election campaigns are.

We believe strongly that the time to engage in meaningful reform of our markets is precisely now – while we still have calm, low-volatility markets. Too often the alarms sound after horrible stress events, and after investors lose confidence and flee our equity markets. We have all seen it. As a matter of fact, Ari Rubenstein (GTS, one of the high frequency market makers on the floor of the NYSE), sounded an alarm in his testimony yesterday:

“In some ways the markets are a bit untested,” Rubenstein said at a House Financial Services Committee hearing on U.S. equity market structure. “It’s definitely something we should talk about to make sure industry participants are prepared in those instruments.”

Rubenstein noted that the ETF market has swelled from $400 billion to $3 trillion in the last decade. He pointed the August 24th ETF crash and said:

“We should take note of the fact that we’ve never seen a high volatility environment with this amount of investment dollars in ETFs, and I think we should be paying attention to making sure markets function really well,” Rubenstein said in an interview following the hearing. “Let’s say there was a mass exodus of positions in ETFs. That’s going to stress the system, and we are going to depend on electronic market makers to provide that liquidity.”

We can only hope that his words and warnings do not prove to be prophetic, and that we have the collective wisdom to reform our markets while we have the chance.