16

May, 2016

16

May, 2016

Read The Footnotes

We read a lot of market structure academic papers and often end up poking holes in them for various reasons including poor data sets and conflicted industry sponsorship. We like to point out these conflicts because many of these papers are often touted by the pro-high frequency trading crowd as evidence that they are not doing anything wrong. A new academic paper titled “Phantom Liquidity and High Frequency Quoting” written by four assistant professors from three different universities has just been published and we discovered that it contains a giant red flag that should not be ignored.

Before telling you what the red flag is, we want to quickly review the paper. In short, the paper examines a 2012 Nasdaq data set in order to analyze the frequency of cancellations to determine if there really is such a thing as “phantom liquidity”. We believe that anybody that has traded a stock over the past few years will tell you that phantom liquidity is not a theory but a fact. But the authors wanted to run the data and analyze the results.

The authors concluded:

“We have analyzed a large data set to shed light on the behavior of HFTs surrounding high levels of cancellation activity. We have found evidence that the only thing occurring during these events is that HFT firms seek the correct price level. This is good for the market. It means that HFT firms process information and help improve price discovery without the need for intermediate executions.”

Yes, you read that right. The authors claim that high cancellation rates are actually good for the market because they aid in short term price discovery since HFT’s are simply adjusting their quotes in response to new information so that they can continue to just capture the bid-ask spread. Here is what they believe:

“One cancellation simply leads to a flurry of them as HFTs all react quickly to new information. No executions occur before the new equilibrium price level is achieved. The HFTs process the information so quickly that price discovery comes from the cancelations rather than from executions. This is the more effective method, since no dollars need change hands.”

The authors determined this by searching for “cancel clusters” in their data and found that these “clusters largely appear to be HFTs sparring with one another to get to the front of the limit order queue, rather than HFTs trapping unsuspecting investors into bad executions.”

Ok, that’s enough of this paper’s theories, time to poke some holes:

First of all, the paper only analyzes data from NASDAQ from 2012. How can any conclusions be drawn when only one of the 12 exchanges data has been analyzed? The way to fully analyze the data is to compile information from ALL 12 exchanges. And this doesn’t even include over 40 alternative trading systems which comprise almost 40% of the volume. Analyzing just one exchange’s data is clearly insufficient and represents a deep lack of knowledge about the equity market.

More importantly, there is a giant red flag in this paper that we discovered by reading the one and only footnote from the paper. Since HFT’s love to say that they focus on the data and not anecdotal evidence, we always like to see where and how these types of academic papers get their data. Here is what the authors say about their data:

“Our dataset contains every message about activity in the NASDAQ limit order book. These messages include all additions, cancelations, and executions and are time-tamped to the nanosecond, so that we have an exact timing and ordering of all messages. The dataset is 5.78 terabytes of data in roughly 125,000 ticker-day files (i.e. one file per ticker per date) and was given to us by an HFT firm.”

Wait, did they just say that the data was given to them by an HFT firm and was not sourced directly from Nasdaq? Yes they did and they provided a footnote::

“We would like to thank Xambala, Inc., which collected the data at their co-located server, nanosecond time stamped it, and processed it into easily an usable format. Without their help, this research would not have been impossible.”

Xambala? Who the heck is Xambala? According to their website, they are a Silicon Valley-based high frequency trading firm that wants to “democratize capital markets”:

“Xambala is one of the fastest growing electronic liquidity providers to capital markets. Our mission is to drive fair, open, and highly accessible markets. We enable rapid price discovery by providing liquidity at the best possible price, quickly.”

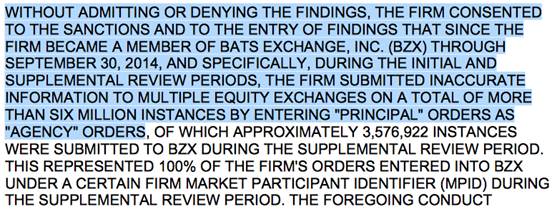

We ran a broker check on Xambala Capital and found a few disclosure events from December 2015 which were centered around Xambala entering orders as agency when in fact they were principal orders:

This behavior violates Section 17(A) of the Securities Exchange Act of 1934 and ended up costing Xambala $95,000 in fines.

In addition to drawing conclusions from only a small subset of data, this academic report used data that was sourced from an HFT firm that has a record of being fined for SEC violations. Clearly, this paper has many deficiencies which is why we give the paper the grade of “F”.