24

Dec, 2015

24

Dec, 2015

What Is Fair?

“If you’re traveling the north country fair

Where the winds hit heavy on the borderline

Remember me to one who lives there

For she once was a true love of mine.”

If December has been All IEX All the Time, and you are a tad weary, we understand. However, please forgive us if we remain on this topic; IEX’s exchange application is the biggest market structure issue / litmus test/ any of you will see in your careers. The comment letters tell you this. NASDAQ has weighed in with a heavy hand, as has NYSE, and has BATS twice. One of BATS’ owners – Citadel – has weighed in twice. Modern Markets has weighed in. Modern Markets Member – Hudson River Trading – has weighed in. Larry Tabb has weighed in. Peter Kovac, the author of Flash Boys – Not So Fast, is the likely author of one of the anonymous comment letters. Russel Investments, Capital Group, and many other buyside firms representing long term investors has also weighed in. IEX has responded several times as well, to clarify misconceptions raised in some of the critical letters by competing interests.

You know what’s funny? Stock exchanges and high speed traders have consistently denied that there is anything called latency arbitrage repeatedly in the past. Manoj Narang, who is profiting handsomely off a system he sells and leases to the SEC, denied it here.

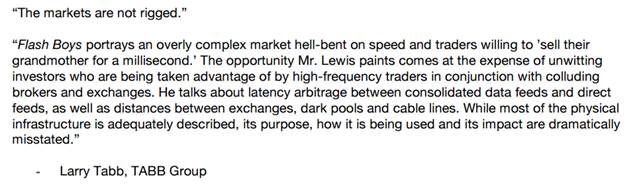

Larry Tabb denied it in 2014 here:

Direct Edge’s Bill O’Brien denied it on CNBC. We would go on, but the list of who denied the existence of latency arbitrage is long.

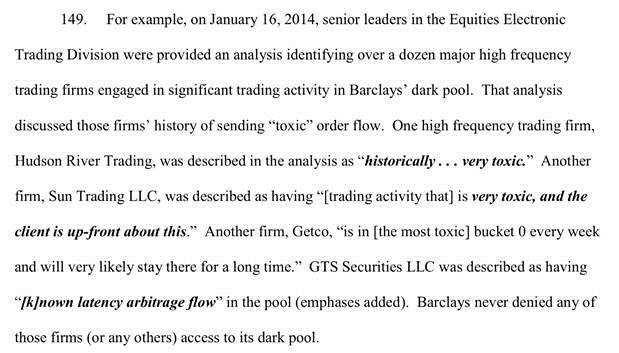

Today, at the end of 2015, everyone finally acknowledges that it exists. Jeff Alexander and Linda Giordano prove that it exists. The Barclays Lawsuit proves it exists:

Twitter has been on fire discussing the IEX application, as has Tabb Forum, which seems to enjoy featuring David Weisberger’s views on IEX quite often.

And Bloomberg’s Matt Levine has weighed in numerous times with well-written Bloomberg articles that layout and summarize points of unfairness that IEX’s exchange application represents – for those embedded in the status quo. Levine has again weighed in quite prolifically – yesterday – in this article: The Flash Boys Exchange Is Still Controversial. Give the article a good read; we are not going to go point- counterpoint with the article, as it’s been done by us, as well as by IEX in their comment letters.

We do want to boil down this exchange application litmus test as simply as we can.

- There is nothing “fair” about trading now, or ever in the past. It’s just a question of who gets to benefit. Latency Arbitrage Exists And Always Has.

- High Speed players post bids and offers in many places at the same time, with the intention of adjusting/fading their quotes on most venues when it gets executed on the first venue. Maker Taker rebates incentivize this behavior.

- Exchanges sell speed (data feeds, colocation, microwaves, lasers, fpga, etc), and it is a dominant source of revenue for existing stock exchanges. Since the turn of the millennium, existing exchanges has learned they can make incredible sums of money by delivering benefit to high speed traders and intermediaries.

- The SEC, despite language in the Exchange Act, and in their mission statement (when the interests of short term traders conflict with the interests of investors, the interests of investors must prevail) has allowed the markets to morph away from the interests of investors.

- IEX has recognized this, and has introduced a free market solution, complete with good marketing, that slows down trading in general to neutralize the speed wars. IEX has created a system that benefits investors in two very large ways:

- If you rest on IEX, because of its 350ms POP, when aggressive “takers” interact with you, more often than not you benefit from a better price by not being executed versus a stale quote.

- If you use the IEX router, as its router does not go through the POP, you get to be the aggressor and “buy what you see across many exchanges” more effectively, and those resting on the other exchanges – particularly high speed players (see point 2), don’t get to get out of the way and benefit off your signal. IEX charges 1 mil (1/100th of a penny) for this service.

- IEX’s solution is fairer for you (investors), than it is for high speed players. Their solution allows you to neutralize billions of dollars of infrastructure set up to disadvantage you, without your making vast capital expenditure outlays on your own, so that you can concentrate on picking investments, and not avoiding trading landmines.

- IEX’s solution neutralizes a great deal of the advantages that the existing exchanges sell. Hence, you see the very dramatic pushback from the status quo.

- Can the SEC create a system that is fair for everybody all the time? We believe they can come close if they could start from scratch. But they can’t.

- Can the SEC allow a new choice where the market can judge success or failure? Has the SEC allowed all of the choices and innovations that “make it fair for the others”? Couldn’t they allow a choice that “makes it fair for you”?

There is much detail in the IEX exchange application debate. Intentional device. Unintentional device. However, there is Exchange Act language that even allows the SEC to “go back on Reg NMS’s “intentional device” language:

Act of 34

SEC. 11A. (a)(1) The Congress finds that—

(A) The securities markets are an important national asset which must be preserved and strengthened.

(B) New data processing and communications techniques create the opportunity for more efficient and effective market operations.

(C) It is in the public interest and appropriate for the protection of investors and the maintenance of fair and orderly markets to assure— economically efficient execution of securities transactions; fair competition among brokers and dealers, among exchange markets, and between exchange markets and markets other than exchange markets; the availability to brokers, dealers, and investors of information with respect to quotations for and transactions in securities; the practicability of brokers executing investors’ orders in the best market; and an opportunity, consistent with the provisions of clauses (i) and (iv) of this subparagraph, for investors’ orders to be executed without the participation of a dealer.

(D) The linking of all markets for qualified securities through communication and data processing facilities will foster efficiency, enhance competition, increase the information available to brokers, dealers, and investors, facilitate the offsetting of investors’ orders, and contribute to best execution of such orders. (2) The Commission is directed, therefore, having due regard for the public interest, the protection of investors, and the maintenance of fair and orderly markets, to use its authority under this Reg NMS Adopting Release Page 19

But when the interests of long-term investors and short-term traders conflict in this context, the Commission believes that its clear responsibility is to uphold the interests of long-term investors.

What is fair? There is no fair for everybody. It’s just a question of “fair for who.” Shall the SEC allow a solution which is fair for you, as opposed to fair for stock exchanges, high speed traders, and arms dealers in general? We think it is time for the SEC to remember “the girl who lives there… who once was a true love of theirs.”