31

Aug, 2016

31

Aug, 2016

The Speed Bumps Are Coming

As expected, once IEX was approved as an exchange, other exchanges have started to introduce their own variation of a speed bump. Last week we discussed Nasdaq’s new Extended Life Order and questioned that there might be more behind their intentions than just investor protection. This week, the Chicago Stock Exchange (CHX) filed their version of a speed bump called the Liquidity Taking Access Delay (LTAD) .

Details of CHX Bump

Here is how the CHX explains their proposed speed bump:

“The Exchange proposes to adopt the CHX Liquidity Taking Access Delay (“LTAD”). LTAD is designed to neutralize microsecond speed advantages exploited by low-latency market participants engaged in latency arbitrage strategies that diminish displayed liquidity and impair price discovery in national market system (“NMS”) securities. In sum, LTAD would require all new incoming single-sided orders received during the Open Trading State that could immediately execute against one or more resting orders on the CHX book, as well as certain related cancel messages, to be intentionally delayed for 350 microseconds before such delayed messages would be processed by the Matching System. All other messages, including liquidity providing orders (i.e., orders that would not immediately execute against resting orders) and cancel messages for resting orders, would be immediately processed without delay. LTAD will not delay any outbound messages or market data.”

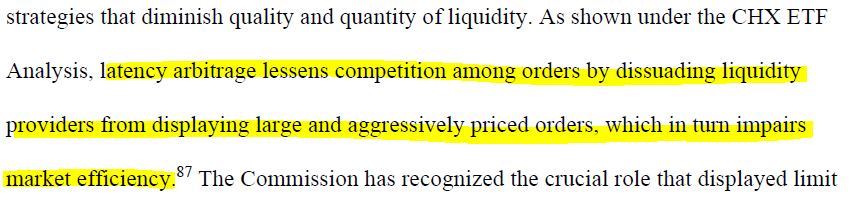

“The Exchange believes that the best way to minimize the effectiveness of latency arbitrage strategies on CHX with respect to resting limit orders is to implement an asymmetric delay, such as LTAD, to deemphasize speed as a key to trading success.”

Basically, the CHX is saying that any order that would immediately take liquidity from its book will be delayed by 350 microseconds. Any other order that would not immediately interact with their quote will not be subject to the speed bump.

Why is the CHX introducing this type of speed bump?

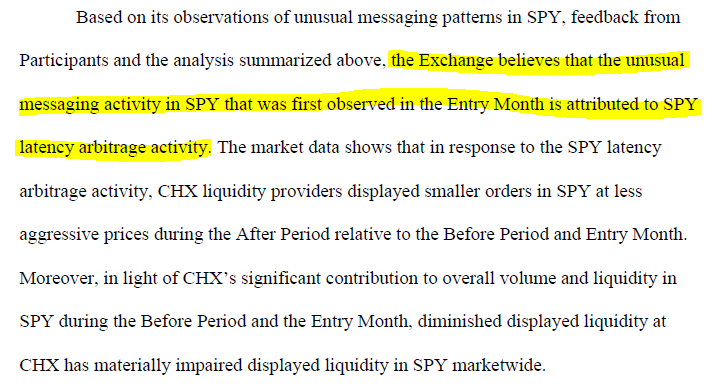

Apparently, in January of this year, the CHX noticed a substantial increase in latency arbitrage activity in the SPY ETF which caused their market share in SPY to drop dramatically (the market share of SPY for the CHX went from 5.7% in January to 0.57% in July). According to the CHX, the latency arbitrage activity was triggered by an “away market event (e.g., change in market data from a futures market) where the liquidity taker is able to take a resting order at a stale price before the liquidity provider could adjust the resting order to accurately reflect the market.” In their proposal, the CHX clearly states that latency arbitrage (which many HFT proponents still deny exists) is real and is harming the market:

Is the CHX speed bump similar to IEX?

No, the IEX speed bump is non-discriminatory and applies to all orders and market data (symmetric). The CHX bump only applies to liquidity taking orders (asymmetric) and will not delay any outbound messages or market data. It is actually very similar to a speed bump that Nasdaq tried to introduce on their PSX exchange back in 2012. Nasdaq’s proposal would have instituted a five millisecond delay in the time between when a marketable order is received and when it is presented for execution. For unknown reasons, Nasdaq subsequently withdrew that proposal.

Is the CHX speed bump similar to the speed bumps that have recently been introduced in Canada?

The Canadian market has already experienced different types of speed bumps. Aequitas has a non-discriminatory bump similar to IEX’s but TMX Alpha unveiled a discriminatory speed bump where certain post-only orders could bypass the bump. Canadian regulators approved the TMX Alpha market in 2015 but took issue with its discrimination and only approved the venue as a non-protected venue which would not fall under their order protection rule.

Our concerns about this new speed bump:

1) The speed bump is discriminatory since it is only applied to orders that would immediately take liquidity. Most likely it was designed to assist electronic market makers in not getting picked off by other high speed traders.

2) Will it encourage quote fading? The CHX thinks their speed bump will “encourage liquidity providers to resume posting large aggressively priced orders on the CHX book”. They believe that their speed bump will “neutralize the speed advantages utilized by latency arbitrageurs.” But could the bump actually exacerbate quote fading if market makers start to cancel orders anytime they feel the market is about to tick against them and if they assume an inbound order is less than 350 microseconds away? Will the delay act similar to a “flash order” which gave market makers the free option to trade or not to trade?

3) The CHX is relying on the IEX approval as precedent for their speed bump and cite that the rule change would be consistent with Reg NMS and would constitute a “de minimis intentional access delay”. However, as we described above, the CHX speed bump is different from IEX. When the SEC issued their guidance on automated quotations in June, they left themselves plenty of room to disapprove any new access delays if they felt they were discriminatory or a burden to competition:

“This guidance does not obviate the requirement for any proposed intentional access delay to be filed with the Commission as a proposed rule change, and it does not address whether any particular access delay would be approved by the Commission as consistent with the Commission’s interpretation regarding automated quotation under Rule 600(b)(3) of Regulation NMS, or as being not unfairly discriminatory, not an inappropriate or unnecessary burden on competition, and otherwise consistent with the Act.”

4) The new CHX speed bump does not help fix our broken market structure. Reg NMS introduced fragmentation to the markets but at the time it was lauded by regulators as a significant enhancement to competition. This fragmentation has since encouraged exchanges and other market venues to develop new order types, fee schedules and speed methods which have turned the simple process of buying and selling a stock into an extremely complex event. High speed market participants continue to take advantage of these structural issues caused by fragmentation and continue to create new arbitrage opportunities based on latency, venue and fee structures.

We sympathize with the CHX and understand that the goal of their proposed speed bump is to encourage more displayed liquidity in certain high volume ETF’s. Driving more volume into the lit quote and out of the dark is good for price discovery but we fear that the CHX solution, if extended to regular stocks, may encourage more flickering stock quotes and enable more spoofing.

We’re sure the SEC was expecting that other exchanges would soon file speed bumps and it will be interesting to see how they respond to this proposal. Will they say it is discriminatory and therefore does not meet its automated quotation guidance? Will they do something similar to what the Canadian regulators did and approve the speed bump but reclassify CHX as an unprotected quote? We’re not sure but we do know that how the SEC acts on this proposal will be precedent setting for any future speed bump proposals.